Online Store

Online Store

Introduction

Over the last several decades, governments have collectively pledged to slow global warming. But despite intensified diplomacy, the world is already facing the consequences of climate…

Carney’s Forward Garble

August 20, 2013 10:27 am (EST)

- Post

- Blog posts represent the views of CFR fellows and staff and not those of CFR, which takes no institutional positions.

More on:

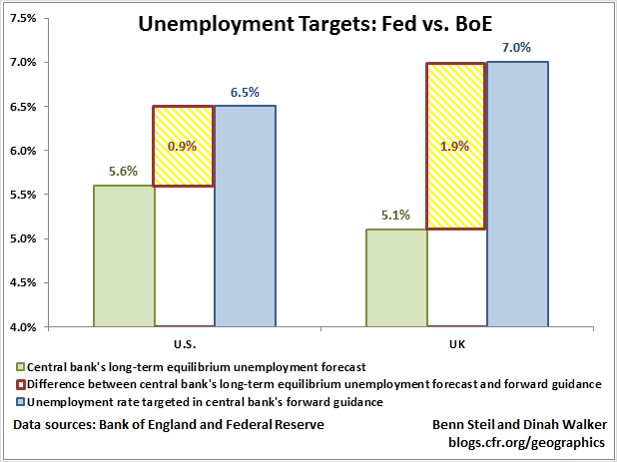

The Bank of England’s dramatic new “forward guidance” policy, announced on August 7 with great fanfare, struck the markets like a soggy noodle – the FTSE fell, gilts fell, and sterling rose, none of which could the Bank have wanted to see.

Why the disappointment? Others have pointed to the multiple caveats and exit clauses, but we would highlight something much more tangible: the pledge to keep interest rates super-low at least until unemployment fell to 7% was meaningless, as 7% is nearly two full percentage points over what the Bank considers to be the long-term equilibrium rate of UK unemployment. This is like a football coach pledging to keep throwing the football until his team is down by less than 50 points; it tells the defense nothing it didn’t already know.

Compare the BoE’s rate pledge to the Fed’s rate pledge, which has the latter committing to a near-zero policy rate until unemployment falls to less than a percentage point above what the Fed considers to be the long-term equilibrium rate of US unemployment. While hardly shocking, the Fed’s commitment was newsworthy.

If a 7% unemployment target was the best that new BoE Governor Mark Carney could deliver through his Monetary Policy Committee, he would have been better advised to skip the forward guidance and simply let the market judge his actions going forward.

Bank of England: August Inflation Report

The Guardian: MPC Member Failed to Back Carney Over Forward Guidance

The Economist: Guidance on Forward Guidance

Financial Times: Carney Ties UK Rates to Jobs Data

Follow Benn on Twitter: @BennSteil

Follow Geo-Graphics on Twitter: @CFR_GeoGraphics

More on: